Types of Protective Life Insurance

Protective made Forbes Advisor’s list of the best life insurance companies and offers these types of life insurance products:

- Term life

- Whole life

- Universal

- Indexed universal life

- Variable universal life

Protective’s Term Life Insurance

Term life insurance is ideal for people who have a specific period they wish to cover with fixed premiums. For example, if a person wants enough coverage for income replacement if they die, a term life policy with a term that covers the remainder of their working years is ideal. Term life insurance is often the least expensive life insurance option but does not build cash value.

Protective offers the Protective Classic Choice Term life product for people ages 18 to 52 seeking term life insurance. You can choose term periods from 10 to 40 years in coverage amounts ranging from $100,000 to $50,000,000. These term life policies are renewable until age 90, but you should prepare for increased premiums upon each renewal.

Protective’s Whole Life Insurance

If you have a whole life insurance policy, a death benefit is guaranteed as long as you pay your premiums, no matter how long you live. Whole life insurance policies offer the perk of building cash value with a guaranteed rate of return and the assurance of premiums that do not change. You can borrow against the cash value of your whole life policy for any reason.

Protective Non-Participating Whole Life Insurance is a policy that does not pay cash dividends like some other whole life policies. The premium, death benefit and cash surrender amounts are set at a fixed amount when you buy the coverage. It is available for people up to age 90. This policy has death benefits starting at $1,000 or $100,000, depending on your health and risk classification, and go up to over $1 million.

Protective’s Universal Life Insurance

Universal life insurance offers coverage that can last a lifetime, depending on the type you choose. Some types of universal life insurance offer level death benefit periods (including a lifetime option) where premiums and death benefits do not change.

If you choose universal life with cash value accumulation, you can withdraw or take loans from the cash value for any reason.

Protective Custom Choice UL offers flexible low premiums without cash value accumulation and is available to buyers ages 18 to 85. With this type of UL policy, one can choose a death benefit level period of 10, 15, 20, 25, or 30 years, or lifetime. During this time, premiums and death benefits remain level or unchanged.

Unless you’ve selected the lifetime option, after the initial level period, premiums will continue to remain level but your death benefit will decrease each year until it reaches $10,000, at which times the premiums will begin to increase.

Death benefit coverage amounts begin at $100,000 and go up to over $1 million.

Protective’s Indexed Universal Life Insurance

Indexed universal life insurance is an option for people looking for cash value that will grow with an index, like the S&P 500, and the flexibility to vary premium payments.

Participation rates and caps on the cash value growth, along with fees, are commonly associated with indexed universal life insurance products.

Protective Indexed Choice UL is Protective’s indexed universal life product available to buyers ages 18 to 75. With this policy, you can choose two interest-building accounts. One option is a fixed account where the interest rate will never fall below 1%, and the other option is an indexed account where cash value can rise or fall based on the performance of the S&P 500. The fixed account is less risk and less return, while the indexed account is a higher risk with a higher potential for return.

Indexed accounts have a guaranteed minimum floor rate of no less than 0%, which means that the interest rate your cash value earns can never fall below 0%, protecting you from losing value due to poor S&P 500 performance. You can, however, lose value as policy fees are deducted from the account.

After your first year as a Protective Indexed Choice UL policyholder, you can transfer funds between your fixed and indexed accounts. You can also access your cash value through a loan or withdrawal for any reason.

Protective’s Variable Universal Life Insurance

Variable universal life insurance may be ideal for people seeking ultimate flexibility. With this type of policy, you can vary premium payments and death benefits. The cash value component is tied to multiple sub-accounts that you get to select.

There is a fixed account option with a guaranteed minimum interest rate for those seeking a little bit lower risk. Like other types of universal life insurance, variable universal gives you the protection of borrowing or withdrawing money from your cash value whenever needs arise.

For example, Protective’s Protective Strategic Objectives II VUL is available to buyers ages 18 to 90 and offers face amounts beginning at $100,000. The fixed cash value account option has an interest rate guaranteed not to fall below 1%. The variable account option gives you the choice of investing in one of four asset allocation portfolios (conservative, moderate, growth & income, aggressive growth) or if you’re interested in choosing your investments, you can invest in a customized portfolio where you select all your investment sub-accounts.

The minimum loan or withdrawal amount for the Protective Strategic Objectives II VUL is $500, and the maximum is 99% of the policy’s cash value.

This Protective life insurance policy comes with some built-in lapse coverage, which gives you a lapse grace period if, on any monthly anniversary, the surrender value is less than the monthly deduction. The grace period gives policyholders 61 days to pay past-due deductions before the policy lapses.

How Much Does Protective Life Insurance Cost?

Protective’s Classic Choice Term costs an average of $127 a year for a 20-year, $250,000 policy for a healthy 30-year-old female, based on our analysis. That’s lower than most other top companies’ rates.

Protective’s Term Life Insurance Rates Compared to Competitors

| Company | Term life insurance policy name | Cost per year: Female buyer age 30, $250,000 for 20 years | Cost per year: Male buyer at 30, $250,000, 20 years |

|---|---|---|---|

| Classic Choice Term | $127 | $144 | |

| PL Promise Term | $128 | $145 | |

| Term Essential | $168 | $185 | |

| TermAccel | $134 | $152 | |

| Guaranteed Level Term | $173 | $180 | |

| Term Life Answers | $155 | $170 | |

| Non-Convertible Term | $127 | $145 |

Protective’s Term Life Insurance Rates by Age and Amount

| Coverage | Buyer age 30, cost per year | Buyer age 40, cost per year | Buyer age 50, cost per year |

|---|---|---|---|

| $500,000, 20-year term life insurance | Female: $186

Male: $221 | Female: $282

Male: $334 | Female: $641

Male: $817 |

| $1 million, 20-year term life insurance | Female: $276

Male: $349 | Female: $476

Male: $573 | Female: $1,127

Male: $1,518 |

Protective’s Life Insurance Riders

Life insurance riders give you the flexibility of customizing your policy with extra coverage or features. Rider availability may vary by policy type. Here are the riders offered by Protective.

- Accidental death benefit rider. This rider may be an ideal solution for someone seeking coverage above their base policy limit for accidental death coverage. Perhaps you work in a dangerous job, and buying additional coverage on your base policy is too pricey. Protective’s Accidental Death Benefit rider offers that additional coverage at an affordable cost.

- Child life insurance rider. You can purchase Protective’s Children’s Life Insurance rider as an add-on to a term life policy. This rider lets you add all children ages 15 days to 25 years for life insurance coverage.

- Chronic illness rider. Protective’s ExtendCare offers you access to your death benefit if you’re chronically ill.

- Conversion choice with chronic illness rider. This rider lets you convert to a broad range of permanent policies and offers a chronic illness rider at the time you convert.

- Disability rider. If you purchase this rider and become disabled, as defined by Protective’s rider requirements, you can receive a percentage of your life insurance policy face value monthly.

- Guaranteed insurability rider. Perhaps you’re buying life insurance now but can’t afford the amount of coverage you truly need. This Protective rider allows you to buy additional coverage at a later date without having to jump through any insurability hoops.

- Income protection rider. This rider provides income (in addition to the death benefit) to beneficiaries after the insured person dies, based on what the person’s regular income was.

- Lapse protection rider. Some Protective Life universal policies come with a built-in no-lapse guarantee. Still, for those that don’t, Protective offers a lapse protection rider so that if there are periods of no or low cash value accumulation, the policy will not lapse even if the cash value is zero.

- Overloan protection rider. If you withdraw or borrow money from your life insurance policy and your surrender value is too low to cover monthly charges, this rider protects you from lapse if certain conditions are met.

- Protected insurability rider.

- Return of premium rider. Protective’s term life policies are eligible for this rider, which refunds the premiums you’ve paid if you outlive the level term period.

- Terminal illness accelerated death benefit rider. If you are diagnosed with a terminal illness, this rider pays out an accelerated death benefit, so you can use the money now for needs you may have. Protective’s rider will specify what conditions must be met to qualify.

- Waiver of premium rider. Protective’s Waiver of Premium rider allows you to stop paying policy premiums temporarily if you become disabled and unable to work. Even though you stop paying the premiums, your life insurance policy will still be in force.

Compare Life Insurance Companies

Compare Policies With Leading Insurers

How Do I Buy Life Insurance From Protective?

How to File a Claim with Protective

You can initiate a life insurance claim with Protective by calling its toll-free number (800) 424-1592 or filling out the form on its website.

Compare Life Insurance Companies

Compare Policies With Leading Insurers

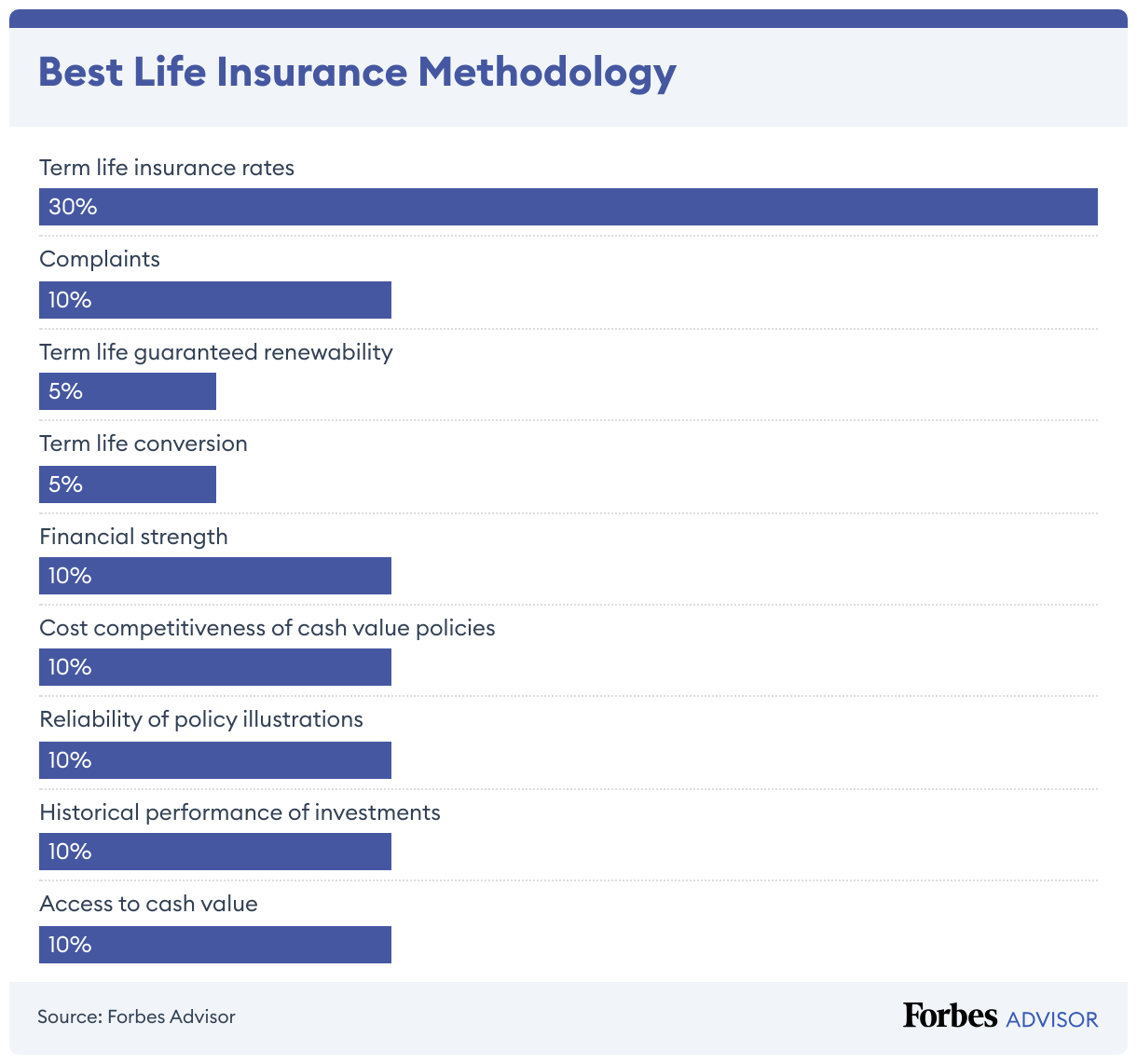

Methodology

To find the best life insurance companies, we evaluated term life and permanent life insurance for each company. We used our own research and data courtesy of Veralytic, a life insurance analytics provider that rates cash value policies based on their overall competitiveness. Veralytic’s data provides a unique depth to Forbes Advisor’s analysis of whole, universal, indexed universal and variable universal life insurance policies from each insurer. Veralytic reports are available through financial advisors.

Our analysis was based on the following.

Protective Life Insurance Frequently Asked Questions (FAQs)

Can I cash out my Protective life insurance policy?

If you have a Protective cash value life insurance policy with sufficient cash value, you can surrender the policy and receive your cash value minus any surrender charge.

You cannot cash out a term life insurance policy as there is no cash value.

Do Protective whole life policies pay dividends?

Protective’s whole life insurance product is non-participating, which means it does not pay dividends.